The choice before the government was to announce it out of the blue and run the risk of the chaos on streets or have a smooth transition from the old currency notes to new notes but without getting much out of it in terms of unearthing unaccounted cash. It has chosen the first, and rightly so.

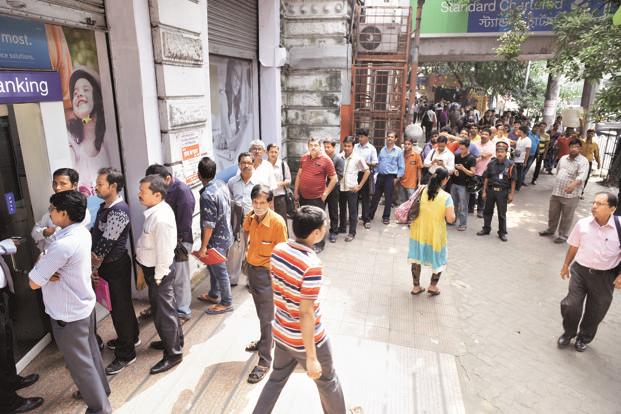

Had I been Kumbhakarna, the younger brother of Ravana in the famous epic Ramayana, woken up in Mumbai last Thursday after a long slumber and looked at the thousands of bank branches that dot the country’s most populous city, I would have thought there’s a run on the entire banking system in Asia’s third-largest economy.

Why were so many people waiting with impatience outside every bank branch? Why were all ATMs closed? Why was the mad rush to withdraw money? Is there a liquidity crisis? Have all the banks gone belly up?

The trigger was the banning of high-value Rs1,000 and Rs500 notes (and replacing them with new Rs2,000 and Rs500 notes over the next 50 days) that took effect at midnight on Tuesday, hours after it was announced by Prime Minister Narendra Modi.

Is there any surprise in the move? Well, unless we were all sleeping like Kumbhakarnas, we should have anticipated it. Bringing back unaccounted money stashed in offshore accounts was a poll promise of the ruling Bharatiya Janata Party. The government gave a three-month window for compliance, but the response has not been great. The next target has been black money within India. The Income Disclosure Scheme 2016 has been relatively successful. It collected Rs65,250 crore, seven times more than what a similar scheme in 1997 had mopped up. A new law to give more teeth to the authorities to curb benami transactions (or transactions done in the name of some person other than the person who has financed it) is also in place. Besides, India’s Double Taxation Avoidance Agreements with Mauritius and Cyprus have been amended.

While all these aim at shrinking the size of the so-called parallel economy, which could be at least one-fifth of India’s GDP, and forcing more citizens to come under the tax bracket, the Pradhan Mantri Jan-Dhan Yojana, a national mission on financial inclusion, launched within months of the new government assuming power, has been trying to expand the reach of India’s banking sector. It has so far opened 254.5 million new accounts, offering access to credit and remittances facility, insurance and pension products to low-income groups.

All these, in stages, created the context for the “surgical strike” of 8 November that attacked black money, fake currency, terrorist financing as well as people’s unwillingness to say goodbye to the cash economy.

Indeed, it has been a logistical nightmare for the banking system. All bank branches remained closed on Wednesday and ATMs for two days, Wednesday and Thursday, but this was too short a notice to prepare the system to meet the demand for new notes. Most ATMs were closed even after two days and bank branches do not have adequate new notes and old Rs100 notes even now. There have been instances of a hospital refusing to release the dead body of a 26-year-old man to his father as he could not arrange the cash in denomination of acceptable currency notes, a newborn baby dying for the same reason, a senior citizen suffering from heart attack while standing in a long queue outside a bank branch to exchange old notes and so on.

Even on Saturday, finance minister Arun Jaitley said it could take as much as two to three weeks for the ATMs to start dispensing new Rs2,000 and Rs500 notes as they are to be recalibrated to accommodate new notes of different sizes. This means the inconvenience of the masses will continue for some more time and political parity of different hues will not end their tirade against Modi’s move.

Shouldn’t this have been handled better? Definitely. At least, this could have come a couple of days later when the Reserve Bank of India (RBI) is ready with the new Rs500 notes. Similarly, Rs100 notes could have been pumped into the system in the run-up to it as that would have made the lives of millions a bit easy. Even if one gets Rs2,000 notes today after a long wait, it’s not easy to use that in the market as the vegetable vendors, provision stores and barbers do not have enough Rs100 notes to return.

However, could this chaos have been avoided entirely? Certainly not. Secrecy is the key to the success of such a move. There was only a three-hour window and even that was wide enough for many with unaccounted money—they bought gold and foreign currency till the wee hours of 8 November, paying as much as 50% premium. Had the government and the Reserve Bank of India (RBI) wanted a foolproof transition by stacking currency chests of all banks with new notes to ensure a smooth transition, the black money hoarders would have got wind and the very purpose of this exercise would have been defeated.

The choice before the government was to announce it out of the blue and run the risk of the chaos on streets or have a smooth transition from the old currency notes to new notes but without getting much out of it in terms of unearthing unaccounted cash. It has chosen the first, and rightly so. My understanding is that the plan was to launch this a bit later, probably in January, but the image of the new Rs2,000 note making the rounds in social media last week unnerved the government and it did not want to take chances with the plan being leaked and instead preferred to launch it immediately, even though the printing of Rs500 currency notes had not even started at that time.

Almost everybody has been discussing how the so-called demonetization (strictly speaking, this is not demonetization—it’s replacing old notes with new) has failed in India and globally and how it could possibly curb only the stock of the black money (that too, partially) and the flow will continue. The habitual offenders would now hoard the new Rs500 notes and the higher-denomination Rs2,000 notes will, in fact, make their job easier. Even now, thousands of Jan Dhan accounts are being ‘sold’—people with unaccounted money are hiring such accounts to deposit Rs2.5 lakh, the limit up to which the tax authorities will not ask any questions on the source of money. There could be endless debates on all these and the disruption in discretionary consumption, gold and property markets, but that does not negate the enormous impact of the historic move.

As of September, the Indian economy had Rs17.3 trillion or $260 billion of currency in circulation, and going by the March 2016 data, Rs500 and Rs1,000 notes contributed to 86% of the value of currency in circulation—around Rs14 trillion or a little over 10% of India’s GDP. Even if a part of this money flows to the banking system and tax is paid on that, the government stands to gain and to that extent, the country’s fiscal health will improve. This will also improve India’s tax-to-GDP ratio of 16.6%, much lower than the emerging markets average of 21%.

On Saturday, Jaitley announced that around Rs1.5-2 trillion fresh deposits flowed into the banking system and the State Bank of India alone has mopped up Rs48,000 crore. In the past one year—between November 2015 and October 2016—the banking system collected Rs8.9 trillion new deposits. At this rate, in 50 days till 30 December, the flow of new deposits would probably be higher than the yearly deposit collection. This will increase liquidity in the system and drive down the interest rates on loans and yields on bonds. The so-called monetary transmission will improve and banks’ profitability too will rise as they will get more low-cost current and savings accounts and their cost of funds will come down.

Indeed, this drive will attack the stock of black money and not the flow, but it will instil the fear of god in the tax evaders the way the new insolvency law will psych the wilful defaulters of the banking industry. The chaos at bank branches and ATMs and people scrambling for new currency notes will also force many to shift to plastic and other channels of payments instead of cash alone. Anecdotally, some of the malls in Bengaluru and Mumbai saw a phenomenal rise in the use of credit and debit cards last week. There will be resistance in rural India, and low-income groups will take time to get used to debit cards, but the combination of the goods and services tax, an Aadhaar-driven financial inclusion and the latest move will change the narrative of India’s formal economy.

However, the immediate challenge before the government and the RBI is to meet the demand for currency. The jute and tea industries in West Bengal have come to a grinding halt; India’s Rs64,000 crore microfinance industry has virtually stopped disbursement of fresh loans and there is pressure on collection of loan instalments; lakhs of people are losing their daily wages as they need to spend hours outside their banks to deposit and withdraw money. All these may lead to social unrest and deteriorating law and order situation in various parts of the country.

The cascading effect of the move can outweigh the gains if not handled properly. Mere congratulations to 1.25 billion Indians and appeal to their patience will not work. Modi may have more plans up his sleeve to fight black money but at the moment, the buck stops with the prime minister.