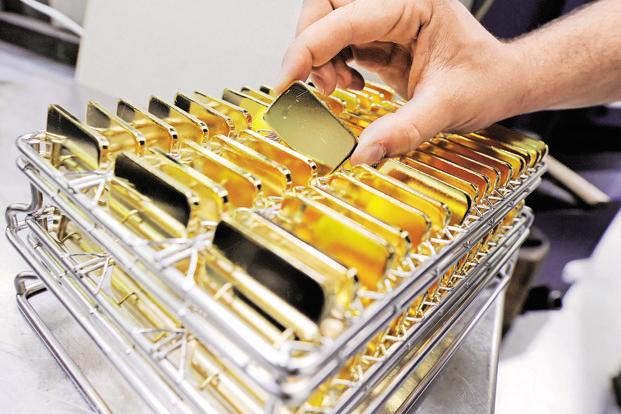

Indians holding gold will now be able to deposit it at commercial banks and earn interest on it. They will also be able to buy bonds backed by gold and earn interest on such bonds instead of owning physical gold itself. Finance minister Arun Jaitley spoke about the gold monetization scheme as well as the gold bonds in his 2015-16 Budget speech in February and the cabinet approved it about a fortnight ago.

The objective is to curb gold imports and, at the same time, develop bullion as an asset class. India imported 915.54 tonnes of gold in 2014-15 against 661.71 tonnes in the previous fiscal year. In the past five years, the average demand for gold has been 895 tonnes annually, roughly one-fourth of the global gold demand.

By the World Gold Council’s estimate, India’s stock of gold could be as much as 22,000 tonnes. It’s no wonder that the cost of India’s gold imports is next only to oil and more than what it spends on importing fertilizer. If the monetization programme succeeds, a large part of the gold stock will be available to the banking system to be on-lent to the jewellers even as the gold bonds will bolster the central bank’s gold reserves.

This is not the first time that India is experimenting with the idea of making productive use of the idle gold. In the past, the government and the Reserve Bank of India (RBI) had tried hard to wean people away from gold without much success. The first gold bond—a 6.5%, 15-year instrument—was floated in November 1962, but it could collect only 16.7 tonnes. The government followed it up with another bond in March 1965 and it could mobilize even less, only 6.1 tonnes. Subsequently, the National Defence Gold Bond scheme in 1980 raised 13.7 tonnes and another gold bond, opened for subscription in March 1993 for three months, mopped up 41.12 tonnes, valued at Rs.1,807 crore at the prevailing price, offering interest of Rs.40 for each gram of gold. Investors could subscribe to this five-year scheme by depositing a minimum of 500 grams of gold and there was no cap on investments. The scheme offered immunity to investors from being asked questions on the acquisition of gold and the source of funds.

Yet another gold deposit scheme was approved by the central bank in 1999, allowing banks to collect gold deposits from the public, but the response has been lukewarm both from the banks as well as their customers. Many of them discontinued the scheme and relaunched it later, but the purpose of making productive use of idle gold has not been served.

Two key recipes for success for such a scheme are amnesty for the investors—something that Jaitley has categorically ruled out—and a relatively high interest rate. Banks are unlikely to offer high rates as they do not earn much by lending gold to the jewellers, and the operational cost for collection, storage and assaying facility for gold is high. Particularly, when gold prices are not moving northwards and bank deposits are offering real returns, after a long time, it will be a challenge to excite investors about gold as an asset class.

The bonds will be issued by RBI on behalf of the government. Linked to gold prices, they will be sold in rupee denominations of five, 10, 50 and 100 grams of gold and the investment is capped at 500 grams annually per person. Carrying a minimum tenure of five to seven years, such bonds can be used as collateral for loans and may be traded on exchanges. The redemption will be based on the prices of gold at that time. These bonds will be part of the government’s borrowing programme and may offer a decent coupon. Of course, the government would need to hedge against the rise in bullion price. In that sense, for the government, it will be akin to borrowing in foreign currency.

The tenure of gold deposits will vary between one-three years to 12-15 years and interest on such deposits will be tax-free. After checking the purity and melting the gold, banks lend the yellow metal to jewellers. Typically, banks offer around 2% to the depositors after factoring in the cost of assaying, storage and transport. Banks run the credit risk and borrowers bear the price risk as they would need to buy the gold from the open market at the time of returning it to the banks. If the banks do not find borrowers after accepting the gold in the form of a deposit, they do not earn anything and the interest cost becomes a drag on the balance sheet. Of course, they can use the gold to meet their statutory liquidity ratio or SLR obligation. RBI would also need to exempt banks’ gold deposits from the reserve requirements to make it attractive for banks.

Theoretically, the gold deposit scheme can develop gold as an asset class and bring down the nation’s import bill, but it will not be easy to tackle 1.2 billion people’s collective obsession with the yellow metal. In 1933, then US president Franklin Roosevelt banned Americans from holding gold and ordered them to sell gold to the government and a failure in doing so attracted a penalty of $10,000 or 10 years of imprisonment. This worked as the US was in the grip of the so-called Great Depression, but the Indian context is very different and we need a different approach to get gold out of household closets.

Banks need to build expertise, target the right customers and educate the masses. For those who have been buying gold coins and bars have already identified bullion as an investment avenue and many of the temple trusts may respond, but the challenge will be to attract those who buy gold jewellery and for whom the yellow metal is an intoxication.