On April 1, the bonds of the Chinese government and its three policy banks responsible for financing economic and trade development and state investment projects were added to the Bloomberg Barclays Global Aggregate Bond Index for next 20 months. Following this, as much as $150 billion could flow into the world’s second largest economy, which has been showing signs of slowdown.

With at least $1.5 trillion of outstanding debt securities, China presents one of the largest central government bond markets in the world. Besides, there are close to $1.8 trillion of policy bank bonds, highly rated by virtue of the government support. A series of policy changes and reforms to woo foreign money has finally started showing results in the third largest bond market in the world, with several important bond indices starting to include China.

Indeed, global bond indices play a critical role in influencing investment decisions and the cross-border flow of debt capital. Such indices guide the fund managers on allocation of investments. When a country gets into such an index, typically foreign funds flow into that country’s bond market surges.

JP Morgan’s Government Bond Index–Emerging Markets Global Diversified Index or EMGDI is the most widely-tracked indices for emerging market debt. China could get into that soon. Once that happens, the flow into Chinese debt will be even thicker.

What about India? Ever since we opened up the capital markets to foreign investors, the flow of debt has been just a little over one-third of equity. There have been many years when the debt flow has been negative. For instance, in the 2014 fiscal year, there was Rs 28,060 crore debt outflow even as the equity market attracted Rs 79,709 crore. Last year, the outflow of debt was even higher — Rs 42,951 crore. In the first fortnight of the current fiscal year that started in April, foreign investors sold Rs 3,288 crore worth of debt.

The key reason behind this is that India, which has been part of the MSCI Emerging Markets Index that measures equity market performance in global emerging markets, has never featured in any debt index as it does not meet the criterion of “free” investment. In 2014, when the country was facing its worst current account deficit and the value of the local currency against the US dollar steeply eroded, the Reserve Bank of India (RBI) discussed with JPMorgan about getting into the emerging market bond index. But, that did not happen because of the strict regulations on foreign investors’ exposure to the Indian debt market in terms of maturity, quantum of investment and the profile of the debt instrument. The scenario has not changed since then.

Launched in November 2008, the JP Morgan Global Aggregate Bond Index (JPM GABI) represents nine distinct asset classes (emerging market treasuries or EMDGI being one of them) and consists of at least 5,500 instruments issued from more than 60 countries, denominated in 25 currencies and collectively representing $20 trillion in market value. Both entry into and exit from such debt instruments are with no strings attached.

The reason for India’s conservatism when it comes to foreign flow into the debt market is the fear of sudden outflow which can create excessive volatility. Even though the equity market was opened up for foreign investors immediately after economic liberalisation in the early 1990s, the norms for foreign investment in debt were released in 1995 and in 1997 Rs 29 crore trickled in.

For fiscal year 2020, the RBI has raised the foreign investment limit in central government bonds to 6 per cent of outstanding stock of securities, from 5.5 per cent in 2019, but the investment limit for both state loans and corporate bonds remains unchanged at 2 per cent and 9 per cent, respectively. In absolute terms, the limit of investment in central government bonds is being raised from Rs 2.23 trillion in 2019 to Rs 2.35 trillion in the first half of 2020 and Rs 2.45 trillion in the second half. Overall, the total foreign exposure to Indian debt is being raised from Rs 6.5 trillion last year to 7.46 trillion this year.

Even this low limit is not utilised by the foreign investors. If we go by the April 1, 2019, data, only 65 per cent of the limit for central government bonds was used. In other categories, the exposure has been far less. Foreign investors’ appetite for corporate bonds is particularly muted, because of the lack of a vibrant second market, among other things.

Opening up of the debt market has always been a sensitive issue. There are arguments both in favour and against it, equally convincing. Many say that we need foreign direct investment and portfolio investment in equities but not in debt as it will complicate an inflation-targeter central bank’s task. How? Once the dollar flow increases, it will strengthen local currency. Similarly, when there is an outflow of foreign money from the debt market, the rupee will be under pressure. This means, the RBI will have to manage the currency.

Also, larger dependence on foreign money will complete integration of Indian debt market with the global markets. This means, if foreign investors want to dump Indian debt to earn more in other markets, the RBI will be forced to tweak the interest rates to keep them happy. That will push up the government’s cost of borrowing. Essentially, an inflation targeter central bank will have to reposition itself into a multi-tasker.

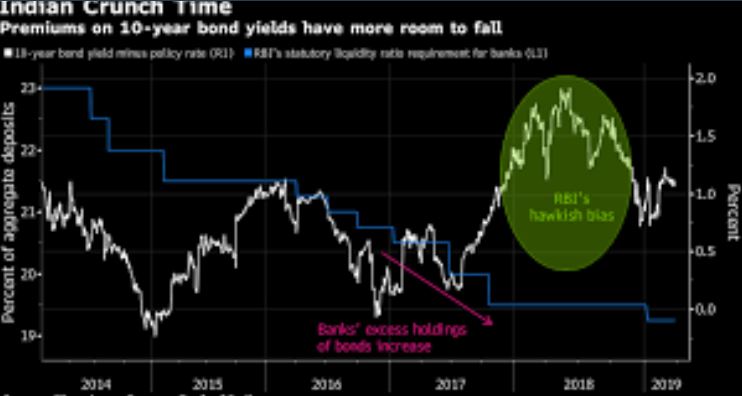

On the other side, increasing presence of foreign investors in the debt market will release the pressure on our banks and free up money for lending. By end December 2018, the banks’ share in the Rs 57.5 trillion central government debt was 40.5 per cent, followed by insurance companies’ 24.5 per cent. Foreign investors’ contribution was a minuscule 3.6 per cent. When it comes to state government bonds, both banks’ and insurance companies’ share was around 34 per cent each and that of provident funds, close to 27 per cent. One would need a microscope to detect the trace of foreign money.

Is it time for the RBI to free up the shackles and encourage foreign investors to dive into Indian debt market? After a difficult 2018, for China, 2019 is the year of the pig — representing luck, wealth, and prosperity — and foreign investors are bracing up to reassess China’s domestic bonds.

Encouraged by the rather unconventional $10 billion dollar swap auctions to increase liquidity in the banking system, will RBI governor Shaktikanta Das shift his penchant for experiment to the debt market after a new government takes over?